Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

This year, respondents said that the fourth greatest challenge to their business was reputational risk for clients in being associated with trust structures and offshore jurisdictions. In this article, we discuss why – six years after the Panama Papers story broke – reputation continues to weigh heavy on trust companies' minds.

It was on 3 April 2016 that the International Consortium of Investigative Journalists ("ICIJ") and its media partners published the first reports linked to the Panama Papers.

Anyone who thought that interest in offshore leaks would quickly be lost in the churn of the 21st century new cycle was mistaken, both as a result of the sheer scale and profile of the Panama story (11.5 million financial and legal records leaked, relating to (amongst others) 140 politicians and public officials from around the world) and the fact that – like a Hollywood franchise – sequels were never far behind: the Paradise Papers came in November 2017, and the Pandora Papers in October 2021.

Indeed, our respondents placed reputational risk one rung higher in the 2022 survey (fourth place) than in the 2020 edition (fifth place).

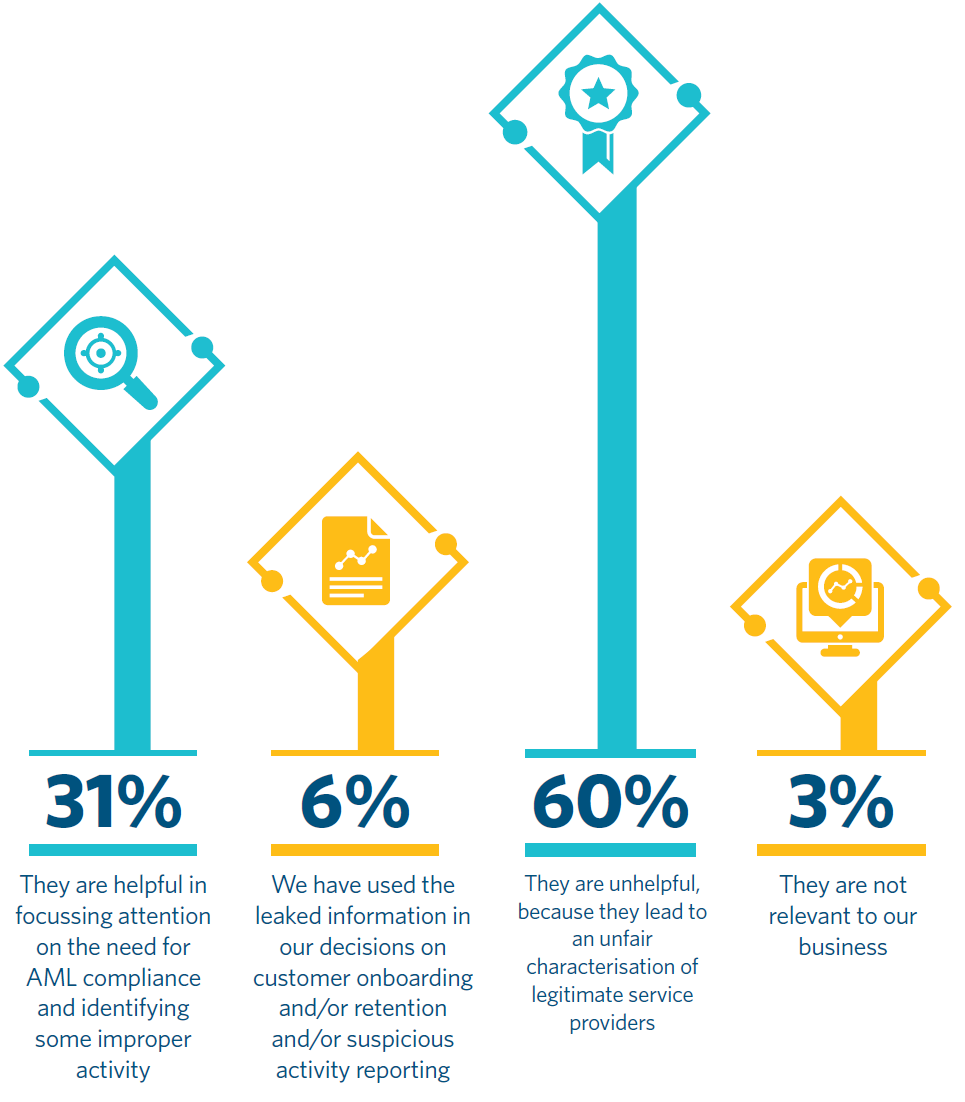

Of those respondents, 31% saw some silver lining in the cloud, and regarded offshore leaks as helpful in focussing minds on AML risk (which will be the subject of an upcoming article). However, a significant majority (60%) was less positive, and regarded the leaks as an unhelpful brush with which legitimate service providers are tarred.

The 'Pandora papers' are the most recent in a series of 'leaks' which have given rise to additional media scrutiny of offshore wealth. Which of the following statements is most true for your organisation regarding these sorts of leaks:

The feeling of unfair characterisation brought about by the offshore leaks ran deep with some respondents, one of whom said that the collections should be referred to as the "Hypocrisy Papers", due to a perceived leveraging of the material by politicians who, as a class, were not immune from involvement in the type of structures being complained of.

This place on the political agenda helps explain why our respondents consider reputational risk to be a key challenge, and we believe that two factors in particular have magnified the attention generated by the ICIJ leaks in recent years: footing the bill for governments' responses to COVID-19, and sanctions imposed following the Russian invasion of Ukraine.

In the UK alone, public spending in 2020/21 was £167 billion higher than planned before the pandemic,1 leading to questions as to how that hole (and those of subsequent years) in the public purse will be filled. Some commentators have suggested the answer lies offshore.

Foreign Policy magazine says that the money to pay for the pandemic is "close at hand" in offshore financial centres ("OFCs") which are estimated to hold up to $36 trillion in "cash, gold and securities", and suggests that leaders now have a chance to "shut down OFCs once and for all" and recover the money owed by the world's wealthy.2 Proposals for doing so include criminalising accountants, lawyers and bankers who create structures "whose only purpose is to minimize or avoid taxes", and enacting attachment statutes to prevent depositors from moving assets when their OFC accounts are revealed.

Similarly, the Tax Justice Network ("TJN") predicts that, in the COVID-19 era, "popular demands for new, radical measures [to bust OFCs] will grow explosively".3 TJN's suggestions for tapping into offshore wealth include: the United Kingdom imposing direct rule on Overseas Territories (e.g. Cayman and Bermuda) and Crown Dependencies (e.g. Jersey and Guernsey) and "close[ing] down their tax haven operations immediately"; and treating trust assets as retained by the settlor until such time as they vest in a beneficiary.

A number of people might say in response that many OFCs (including Bermuda, the British Virgin Islands, the Cayman Islands, Guernsey and Jersey) were among the first adopters of the OECD's Common Reporting Standards, and that they play a legitimate and important role in the globalised economy.

The same article in Foreign Policy magazine estimates that "almost 50 percent of Russian wealth" is held, untaxed, in OFCs. This brings us to a very recent avenue of attack on the industry's reputation: the alleged use of structures to put assets outside the scope of sanctions imposed in response to the invasion of Ukraine.

For example, the UK's Guardian newspaper has reported that Alisher Usmanov, the Russian ultra-high net worth ("UHNW") individual, is connected to UK property worth more than £170 million and a $600 million private yacht, but that a spokesman for Mr Usmanov had said that these assets had "long ago been transferred into irrevocable trusts", potentially putting the assets outside the reach of the sanctions imposed against him.4

Meanwhile, the World Economic Forum says that Western gatekeepers (including accountants and lawyers) have "played an essential role in moving, hiding and investing the very same assets that Western sanctions are presently after", and cites UHNW Russians' use of "blind trusts" and "tax havens" as a means of concealing "massive sums of money".5

In the introductions to both the 2020 and 2022 editions of this survey we discussed the idea of the Black Swan event, and how COVID-19 and the ramifications of the invasion of Ukraine could fall within that description.

It is noteworthy that both of these international issues have led to heightened media scrutiny of offshore trust structures, and it seems that despite increasing regulation, a perceived need to bust the trust will not abate any time soon, and indeed that global crises will intensify the spotlight.

Whilst we do not expect that many of the more radical proposals discussed above will come to pass (and life is rarely as straightforward as the suggestions made), we consider that all the while the narrative remains the same, reputational risk will remain high on trust companies' list of concerns.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2024

We’ll send you the latest insights and briefings tailored to your needs