Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

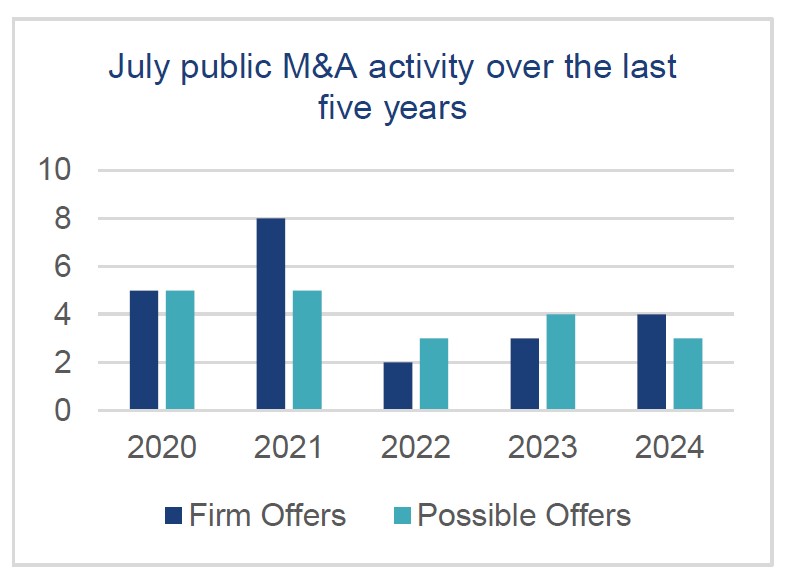

In July 2024, there were four Rule 2.7 announcements made across the UK public M&A market and three further possible offers announced.

New UK Listing Rules in force

The FCA published a Policy Statement (PS24/6) in July 2024 containing the final new UK Listing Rules (UKLRs) to implement the long awaited restructuring of the UK listing regime (proposed in CP23/31). While the genesis of the rule changes is the desire to attract more companies to list in London, they will have a significant impact on existing listed companies.

UKLRs

The new rules, which involve a complete re-write of the rule book, came into force on 29 July 2024 – and obligations in the current rules not carried across to the new UKLRs fell away on that date.

Proceeding with substantially all of the trailed proposals from December 2023 and March 2024, the key changes for companies in the new Equity Shares (Commercial Companies) category are that:

All premium listed companies automatically migrated to the new Equity Shares (Commercial Companies) (ESCC) category; standard listed companies moved to the new transition category; and overseas companies with a secondary listing in London have their own category.

UK MAR and the DTRs continue to apply in the same way and are largely unchanged.

Further information

You will find more detail on the new UKLRs in our three snapshots:

We also discuss the new listing regime in our On the Horizon podcast which you can listen to here.

We also discuss the impact the new rules will have on public M&A in the UK in episode 25 of our public M&A podcast series.

In particular we discuss:

To listen to the full conversation please visit SoundCloud, Spotify or iTunes.

All episodes in our UK public M&A podcast series are available on our public M&A podcast page.

Compensation order and cold-shoulder rulings for breaches of Takeover Code

The Takeover Panel and Takeover Appeal Board have issued a ruling pursuant to which:

The rulings relate to:

Whilst the compensation order relates to a breach of Rule 9, most of the individuals have been cold-shouldered for misleading the Takeover Panel.

This is the first time a compensation order has been made under the powers given to the Panel under section 954 of the Companies Act, and only the fifth time the Panel has used its cold-shoulder powers. No FCA-regulated firm can act for an individual who has been cold-shouldered on any transaction subject to the Takeover Code for the duration of the Panel sanction (ranging in this case from one year to 5 years).

Ordinarily, the Panel Executive would have required a Rule 9 offer to made by the concert party members to the other MWB shareholders. However, as MWB was liquidated in 2013 and then removed from the Register of Companies on 15 April 2018, the Executive took the view that it was impracticable, if not impossible, to restore MWB to the Register with a view to reconstituting the company and requiring the Rule 9 offer. Accordingly, it sought a compensation order as an alternative.

The full detail is set out the Hearings Committee Ruling (PS 2024/16). A summary of the Panel's sanctions is set out in PS 2024/17. The Takeover Appeal Board ruling (TAB 2024/1) related only to the compensation order, rather than the facts or other findings.

We discuss the rulings in our episode 26 of our public M&A podcast series, which you can listen to here.

July 2024 Insights:

The number of firm offers announced this month has increased slightly compared to the previous two years but still lags behind 2021, with the announcement of four firms offers. This year has seen fewer possible offers than last year with three possible offers announced compared to four in 2023. However, the number is comparable to what was seen in 2022. Overall, across the last three years, there is an upward trend in firm offers announced, which could indicate an improving and busier market during the summer months.

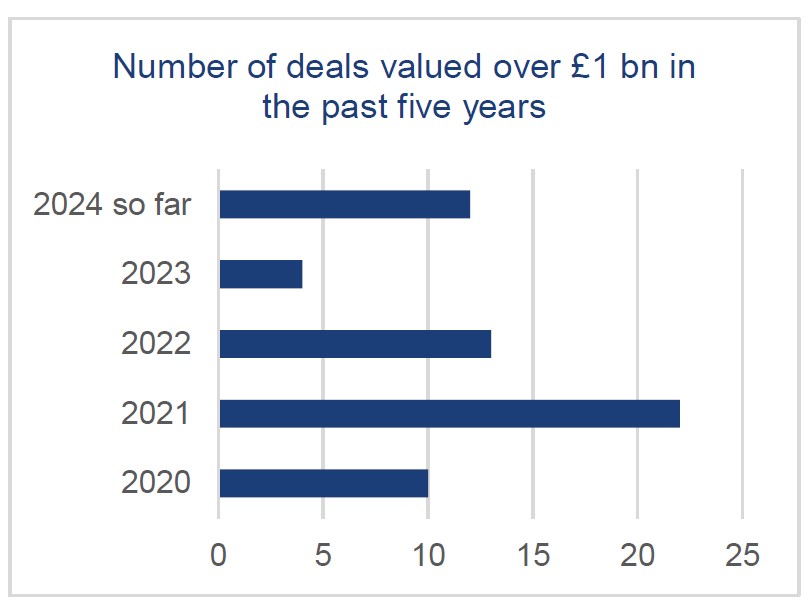

2024 has already seen more deals with a value over £1 billion compared to 2023 – 12 deals have been announced so far with a value over £1 billion in 2024, compared to just four in 2023. Three of these deals came in July: EQT Group made a £2.1 billion offer for Keywords Studios plc; Carlsberg A/S made a £3.3 billion offer for Britvic plc; and Informa PLC's offer for Ascential plc was valued at £1.2 billion. Based on the numbers so far this year, 2024 is on course to have the highest number of deals valued over £1 billion of the past five years, rivalling the bumper year in 2021 which saw 22 deals over £1 billion.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2024

We’ll send you the latest insights and briefings tailored to your needs