Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

This regulatory update provides some observations on key issues arising from the Discussion Paper with a focus on equity capital markets.

The Discussion Paper observes that:

ASIC acknowledges the importance of private capital as both a source of capital for Australian businesses and an investment opportunity for Australians. To the latter point, it notes the emerging importance of superannuation funds in private capital markets. With strong growth and increasing concentration in superannuation funds in Australia, these funds have been increasingly allocating substantial capital to domestic and international private markets (and it is also worth noting that they intermediate, through what are effectively highly sophisticated private capital vehicles, substantial investment in listed and unlisted vehicles for the benefit of their retail clients).

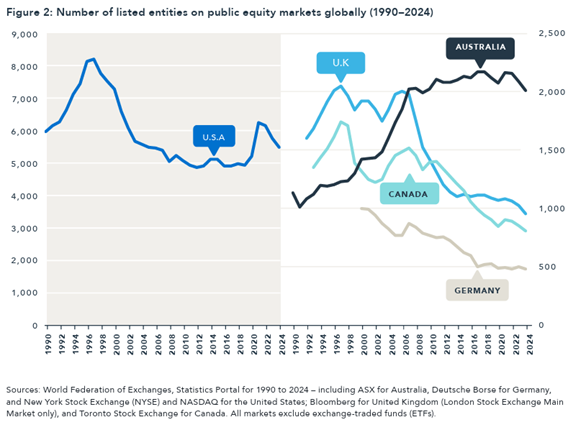

Conversely, the Discussion Paper observes a global decline in net listings on public equity markets. It examines possible factors driving this decline – including:

While the Discussion Paper acknowledges that new listings in Australia are at their lowest level in over a decade, it points out the surprising resilience of Australia’s public market (and specifically notes that, in 2024 when there were relatively few IPOs, the market and potential valuations reached all time highs). This is particularly so when compared with other major markets as illustrated in the below graph. Having said that, the below graph does not show the entire picture and the Report notes that the ASX has reduced its share of global market capitalisation from 1.7% to 1.4% in the last 10 years, primarily as a result of the attractiveness of the NYSE and Nasdaq.

ASIC also highlights the increasing concentration of public markets on a number of fronts, noting that the number of listed vehicles has decreased but aggregate ASX market capitalisation has increased. In addition, ASIC notes the growing influence of index investing and superannuation funds, observing that index funds, with AUM in Australia of more than A$700 billion, may reinforce concentration as they are typically weighted by market capitalisation. It also notes that the “Australian market is concentrated, with most companies in the financials and mining sectors, and less represented in sectors that will drive growth in our increasingly digital future”.

Whether recent changes are cyclical or structural (or both) is a key question considered in the Discussion Paper.

ASIC describes Australian listing settings as ‘attractive’, with a shorter IPO timetable and lower barriers to entry. It concludes that regulatory burden is likely only a small contributor to the decline in IPO numbers, although this appears to us to be a conclusion worth debating further. Report 807 “Evaluating the state of the Australian public equity market: Evidence from data and academic literature”, commissioned by ASIC and released alongside the Discussion Paper, suggests that the decline in listings in Australia is likely to be cyclical, citing the history of listings in Australia, changing global trends, shifts to private markets and the impacts of superannuation.

ASIC states that ‘it is too soon to conclude that fewer net listings in Australia is a sustained trend, but we are concerned’. It acknowledges that the decline in IPOs may be structural in several foreign markets, with the United States being presented as a case study for structural decline in Report 807.

ASIC stresses the importance of having quality, diversity and depth in Australian public equity markets, and notes the importance of public markets as a public good, offering price discovery and transparency, liquidity, efficient valuation and pricing and capital allocation. The health of both public and private markets is said to be ‘crucial for Australia’s economy and overall prosperity’.

ASIC says it is open to exploring changes to regulatory settings to improve the attractiveness of Australia’s public markets, and that it is exploring opportunities with the ASX to refine the listing pathway and listing rules. These comments are helpful and we welcome discussion of concrete steps that can be taken to streamline the listing process, as the length of time during which Australian IPOs are effectively in the public domain has been seen by the industry as a contributing factor to the recent decline in IPO activity.

However, we also think it would be appropriate for ASIC to consider whether there are ways to reduce the volume of ‘red tape’ imposed on companies after listing whilst maintaining the core protections required of public markets, as ongoing regulatory compliance costs and risks and their potential to distract from the operation of a business are potentially a more important factor in deciding whether to list or not than the complexity of an IPO process itself (given the IPO process is obviously very transitory).

It is against the backdrop of growth of private markets, coupled with a downturn in public markets, that ASIC commissioned the Discussion Paper.

With the rise in the significance of private markets, ASIC notes the opacity of these markets as a risk (a point that has also been picked up by APRA and the RBA in previous discussions on the topic) and suggests that this informational asymmetry poses a challenge for investor decision-making and raises questions about appropriate regulatory oversight of private markets.

Alongside opacity, the Discussion Paper identifies as other key risks:

In identifying these risks, ASIC notes that, internationally, foreign regulators have focused on market efficiency and the fair treatment of investors as particular areas of concern affecting market confidence.

While it is acknowledged that private markets may be more opaque and less extensively regulated than public markets, it should be kept front of mind that the regulatory underpinning of this is that access to these markets is restricted to experienced investors who are relatively well equipped to protect themselves. Retail investor exposures are ultimately intermediated by sophisticated fund managers and superannuation funds. The Discussion Paper puts forward the option of ASIC leaving private markets and wholesale investors ‘to their own devices’. It is to be hoped that the Discussion Paper will not result in regulatory overlays which unintentionally reduce market efficiency or the competitiveness of Australia’s private capital markets without substantially enhancing retail investor protection or the overall health of the Australian financial system.

The Discussion Paper calls for industry insights into the opportunities and risks arising from this shifting dynamic between public and private markets and asks for ‘actionable ideas’ for ASIC to consider.

There is a recurrent focus on the scarcity of data available to ASIC and other members of the Council of Financial Regulators (being the RBA, APRA and the Commonwealth Treasury) from which risks can be accurately assessed. ASIC observes that regulatory reporting obligations for private funds ‘lag behind global regulatory best practices’, pointing to the United States, European Union, the United Kingdom and New Zealand as jurisdictions that regularly collect data to better inform their regulators.

ASIC refers to its recommendation to Treasury to introduce a legislative framework for the regular collection of data and asks what additional transparency measures would be appropriate. In the alternative, ASIC asks what other tools are available to support market integrity and fair treatment of investors in private markets.

While acknowledging ASIC’s points, action should not be taken for the sake of taking action. Any change in regulatory settings should be grounded in the balance between the specific risks to be addressed, and the direct and indirect costs of compliance.

The Discussion Paper outlines key global regulatory responses to changes in public and private markets. Of the seven jurisdictions discussed (United States, United Kingdom, European Union, Canada, New Zealand, Hong Kong and Singapore):

There are good reasons to think that ASIC will seek international comity in its response to the issues raised in its Discussion Paper and adopt an approach that is consistent with its peers (and builds on their learned experiences).

On the one hand, we think it is likely that ASIC will look to identify and address barriers to entry to public markets, and would encourage this.

On the other hand, ASIC may seek to facilitate retail investors’ access to private markets while managing the risks discussed in the Discussion Paper, including by subjecting the private market to greater monitoring and oversight, particularly around issues relating to opacity, valuations and conflicts of interest. In particular, we note that some of the firmer comments from ASIC in the Discussion Paper are around ‘ASIC [needing] better recurrent data to more accurately assess risk’ and its views that the health of both public and private markets are essential to Australia.

While initiatives to encourage access to public markets by simplifying regulatory overlay are welcomed, we would urge caution in applying additional regulation to Australian private markets, lest:

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2025

We’ll send you the latest insights and briefings tailored to your needs