Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

Projections from various organisations all show a significant role for gas in the energy mix to meet global energy demand in 2050.

Indeed, gas has widely been seen as a “transition fuel”; a bridge between an economy running on coal vs one running on renewables. However, increasingly the lifecycle emissions of gas as an energy source are being compared to those of renewable energy sources, where gas does not fare as favourably.

Decarbonising gas is therefore unavoidable to ensure a role for gas in the energy transition and to fulfil Net Zero 2050 ambitions.

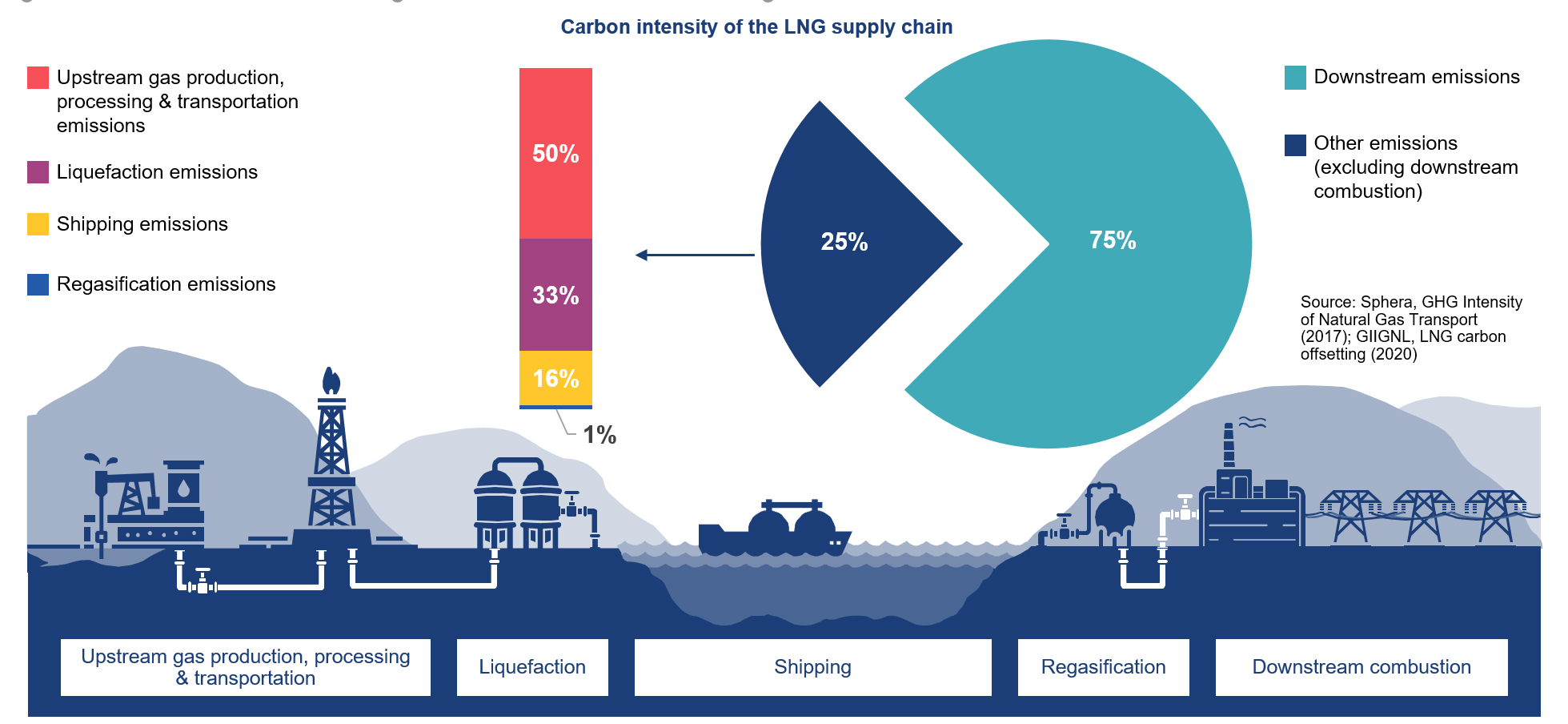

For many countries without domestic gas production or the option of pipeline gas from nearby countries, uptake in gas demand will be met by LNG.

By its very nature, LNG spans continents and involves different industry processes and the emissions from LNG have up until now been considered on this more segmented basis. However there is an increasing focus on the lifecycle emissions of the whole LNG supply chain, which involves carbon emissions along every step of the chain up to final combustion.

Decarbonising the LNG supply chain, however, comes with its challenges.

One main pre-requisite for decarbonisation is a robust emission monitoring, reporting and verification system that provides clear data in order that the emissions footprint of the supply chain can be better understood. However, there is currently no such national or supranational overarching system and with very little data available on emissions across the LNG supply chain, it is difficult to achieve decarbonisation.

The drive for decarbonisation is also slowed by other considerable challenges, such as:

Companies and industry bodies have started to fill the void by developing their own methodologies and setting emissions targets (see, for example, the tender process run by Pavilion Energy – and awarded to Qatar Petroleum in November 2020 - for a long-term LNG supply agreement which required parties to jointly develop and implement a greenhouse gas (GHG) quantification and reporting methodology for emissions).

LNG players essentially have two options to mitigate the carbon footprint of LNG: reduce GHG emissions and/or offset GHG emissions. Transparency of data at each stage of the LNG supply chain from a robust monitoring, reporting and verification system is a prerequisite to both.

A “carbon-neutral” LNG cargo refers to an LNG cargo where its GHG emissions have been reduced to zero or otherwise offset in full. Typically this would take account of the entire product lifecycle GHG emissions (from well to wheel), although there are differences in approach being applied in the market (further reflecting the lack of a robust MRV system).

There are now a number of examples of carbon neutral LNG cargoes being sold in the market (eg. Shell, Tokyo Gas, JERA, ADNOC, Total and CNOOC have all been involved in deals for carbon neutral cargoes). However, the scalability of this model currently looks challenging given the limited size of the offset market and the current cost of offsets compared to relative carbon prices.

For decarbonisation of LNG to take hold, a comprehensive model should be developed to permit financial viability and emission reduction. In order to start producing and delivering what is now being called “advantaged” or “differentiated” gas, technological and regulatory changes have to be implemented at each stage of the supply chain from upstream production to downstream combustion.

While exporting and importing countries have their role to play by expanding their existing regulatory arsenal,1 companies can also lead the way by offsetting the carbon from their LNG cargos2 or exploring other alternatives, for example reducing flaring and venting, using carbon capture and storage and other abatements technologies, and exploring alternative low or zero-emission fuels such as hydrogen. In light of high costs likely to be associated with some of these alternatives, securing funding should be at the heart of companies’ strategies, and it is critical for companies and governments to reorient capital flows towards such investments3 while thinking how the increased costs will be allocated between the different players in the supply chain (including, ultimately, consumers as end users and tax payers).

In order to successfully implement a global decarbonisation strategy of the LNG supply chain a series of outcomes need to occur. These include increased regulation of emissions (including carbon pricing mechanisms), increased access to government support for technologies which currently are not financially viable, international harmonisation of different regulatory regimes to create a level playing field for advantaged gas, and ultimately the political will to share any additional costs across wider society. The growth of the LNG industry over the past decades has in many ways been a real success story, playing a major role in meeting the rising energy demands of the world – but this next chapter and how effectively the industry tackles the issue of decarbonisation may ultimately determine the success of the industry in the decades to come.

For more information, please do not hesitate to contact Lewis McDonald, Partner, Reza Dadbakhsh, Partner, and Eliza Eaton, Senior Associate, and we would be very happy to discuss this further with you.

[1] The EU is leading the way by considering a carbon border adjustment mechanism aimed at shielding selected industries against imports from countries with less strict climate policies and reducing the risk of carbon leakage.

[2] However, offsets have been criticised for continuing to allow emissions and so there is a view they should be used as a last resort.

[3] The EU is also leading the way in this area, having introduced a “green taxonomy” as part of its Action Plan on Sustainable Finance to try to provide a “common language” for classifying environmentally sustainable activities.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2024

We’ll send you the latest insights and briefings tailored to your needs