Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

Although the implementation date for the SFDR RTS has been delayed, large parts of the SFDR regime still apply from 2022.

Rumours had been spreading in the market for the last couple of weeks that the EU Commission would again defer the application of the level 2 provisions of the EU Sustainable Finance Disclosure Regulation (SFDR). With scrutiny by the EU Commission, Parliament and Council still outstanding on the last SFDR RTS draft of 22 October 2021, it was looking increasingly unlikely that the final delegated act would be published sufficiently in advance of the proposed implementation date of 1 July 2022, even without the current disagreements between the EU Commission and Council on the Taxonomy Regulation’s implementing provisions. Accordingly, the EU Commission has announced yesterday that it will defer the application of the SFDR RTS to 1 January 2023.

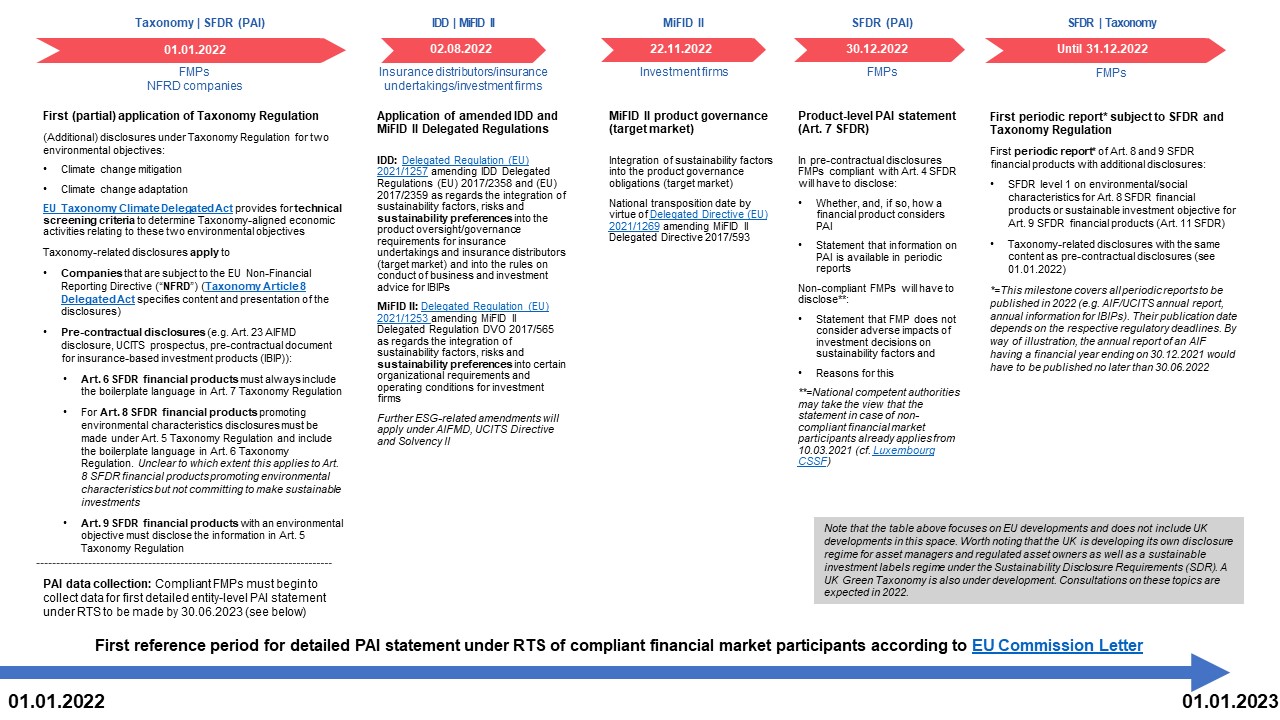

While this may provide some relief to financial market participants (including asset managers, insurers, banks and investment firms) (FMPs) rushing to implement SFDR and other elements of the EU Sustainable Finance Strategy, in reality the respite is all too brief. Even with the deferred implementation of the SFDR RTS, there are numerous significant milestones for FMPs to be mindful of in 2022, as set out below:

Absent further clarification by the EU Commission or the European Supervisory Authorities (ESAs), meeting even the first milestone (pre-contractual disclosure of the share of investments aligned with the Taxonomy Regulation) will remain a challenge for FMPs. These disclosures will include a qualitative element (setting out the relevant environmental objective under the Taxonomy Regulation, if any) and a quantitative element (share of investments in Taxonomy-aligned economic activities satisfying inter alia the level 2 technical screening criteria). However, it is far from clear how the quantitative element can be determined and, in particular, what data may be used for this purpose. Rumours that the ESAs will not allow FMPs to rely on estimates and will require “real data” from target companies or third-party data providers suggest that this task could become even more challenging.

Moreover, FMPs will still need to issue the first periodic reporting for their financial products in 2022, containing the information prescribed by the level 1 provisions of SFDR and the Taxonomy Regulation. The use of the detailed periodic reporting templates provided in the draft SFDR RTS is not yet mandatory, but they do provide some helpful guidance on the type of information required. While many FMPs will probably choose not to disclose some more detailed pieces of information required by these draft templates (e.g., top investments or the complex Taxonomy-alignment calculation based on various KPIs), it would not be surprising if there are at least some examples of periodic disclosures that resemble the draft SFDR RTS templates. Similarly, we expect that despite the deferral, some FMPs will use the pre-contractual templates provided in the draft SFDR RTS as a basis for pre-contractual disclosures going forward (probably in a slightly modified, downsized version, e.g., without the detailed Taxonomy-alignment calculation). In this context, it is important not to forget that the additional disclosures mandated by the Taxonomy Regulation from 1 January 2022 are not limited to financial products according to Art. 8 and 9 SFDR. Financial products subject to Art. 6 SFDR will also need to include certain boilerplate language in their pre-contractual and periodic disclosures.

It is worth noting that the deferral of the SFDR RTS does not have any effect on the new rules on sustainability preferences of customers under the second EU Markets in Financial Instruments Directive (MiFID II) and the EU Insurance Distribution Directive. Those rules will still come into force on 2 August 2022. In the absence of uniform pre-contractual templates, it will become even more difficult to classify financial products as meeting customers’ sustainability preferences. Industry initiatives such as the European ESG Template (EET), designed by FinDatEx for the exchange of broader ESG information, may help but it remains to be seen how useful this will be for distribution networks.

Finally, the EU Commission has clarified in its letter that the deferral will have no impact on the reporting of principal adverse impacts of investment decisions on sustainability factors (PAI) under Art. 4 of the SFDR. The letter confirms that the first detailed report on PAI will continue to be required by 30 June 2023, covering a reference period from 1 January 2022 to 31 December 2022. This means that FMPs complying with Art. 4 of the SFDR will need to start collecting data on PAI from 1 January 2022. This contrasts with the position taken by some national regulators, such as the German BaFin, according to which PAI collection would only have been required from the date on which the SFDR RTS came into effect. Consequently, any projects dealing with the PAI data collection should continue as before and are unaffected by the deferral of the SFDR RTS. To the contrary, it may even be required to speed them up in jurisdictions where the national regulator indicated a later start date. FMPs should also keep in mind the product level PAI disclosure obligations under Art. 7 of the SFDR which will still apply from 30 December 2022. Although there is no regulatory link between the data on PAI indicators collected under Art. 4 SFDR and the obligations under Art. 7 of the SFDR, we expect that for practical reasons most FMPs will use the same set of data for both purposes.

As a result, notwithstanding the deferral of the SFDR RTS, there is still much to do in 2022 which leaves little room for a break. By deferring the SFDR RTS, the EU Commission may have given FMPs more time to meet strict level 2 requirements, but it has also created an even longer period of uncertainty about the final content of the SFDR RTS. Given the many milestones to be met in 2022, FMPs do not really have the luxury to pause their broader SFDR implementation projects and just wait until the final SFDR RTS is published. In fact, the lack of much-required regulatory guidance has the potential to increase inefficiencies and lead to additional implementation costs for FMPs. FMPs should therefore closely follow both regulatory and industry developments over the course of 2022 to reduce the risk of having to make substantial changes to their implementation projects when the SFDR RTS are finally agreed.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2024

We’ll send you the latest insights and briefings tailored to your needs