14 11月 2022

Insight

Australia

Uncertainty regarding the receipt of regulatory approvals is fuelling concerns regarding completion risk.

These concerns are exacerbated by the equity and credit market volatility and weakening economic conditions that we are witnessing.

Against that backdrop, it is timely to consider how the scheme process can unfold where there is uncertainty regarding a regulatory approval process and relevant strategic considerations.

IN BRIEF

Regulatory approval processes in connection with Australian public M&A are a topic of focus for market participants at present.

Where the acquisition of a listed company is being undertaken via scheme, the typical approach adopted is to delay its shareholder vote until all required regulatory approvals have been received (or are at least imminent).

However, there are alternative courses of action that might make greater strategic sense in the circumstances.

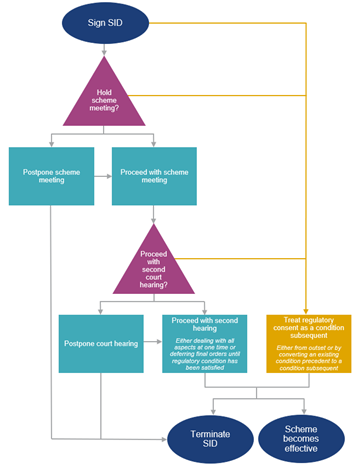

HOW THE SCHEME PROCESS CAN UNFOLD IN THE CONTEXT OF REGULATORY APPROVAL UNCERTAINTY

Parties faced with regulatory approval uncertainty need to decide whether to proceed with the shareholder meeting and the second court hearing notwithstanding the uncertainty.

Set out below is high level overview as to the general courses of action available to the parties when faced with these decisions.

Legal and commercial considerations that may inform each party’s strategy are considered further below.

Postpone the scheme meeting

The typical practice in the Australian market is for a target to delay its shareholder vote until all required regulatory approvals have been received (or are at least imminent), with the regulatory approvals framed as conditions precedent in the scheme implementation deed.

If the approval is not (or it is likely that it will not be) obtained prior to the agreed end date, the parties will need to either extend the end date or the implementation agreement will terminate.

Proceed with the shareholder vote notwithstanding the uncertainty

However, it is open to the parties to proceed with the scheme meeting and have target shareholders vote on the transaction notwithstanding the uncertainty.

This approach was adopted in the 2022 Crown / Blackstone acquisition scheme process, 2017 Tatts / Tabcorp acquisition scheme process, the 2016 Intecq / Tabcorp acquisition scheme process and the 2016 Asciano / Brookfield acquisition scheme process.

Proceed with the second court hearing notwithstanding continued uncertainty

If the shareholder vote is held notwithstanding the uncertainty, the regulatory approval may not be received by the scheduled date for the second hearing, thereby raising the question as to whether the parties proceed with the hearing.

Courts are generally reluctant to approve a scheme that is subject to an outstanding condition. And there may be commercial drivers for deferring the second hearing.

However, it is possible to proceed with the substantive aspects of the hearing only and request that the court defers the making of the final orders for a sufficient period to allow the required regulatory approvals to be obtained and adjourns the hearing until such time.

By asking the court to proceed with the second court hearing but defer the making of final orders, the target may obtain confirmation from the court that it intends to provide the final order approving the scheme if the outstanding approvals are received and abridge the period between receipt of the regulatory approval and completion of the transaction, which can be used to rally support for the transaction.

In addition, the adjourned hearing can be dealt with on the papers, without the need for a further appearance or any further evidence or submissions.

Although uncommon, this was the approach adopted in the 2020 GetSwift redomiciliation scheme process, the 2019 Amcor redomiciliation scheme process and the 2016 Intecq / Tabcorp acquisition scheme process.

Treat the regulatory approval as a condition subsequent, rather than a condition precedent

Finally, the parties can agree that the regulatory approval will be treated as a condition subsequent that can be satisfied after the second court hearing (rather than a condition precedent that must be satisfied prior to that hearing), provided that the court is comfortable with this approach.

As noted above, courts are generally reluctant to approve schemes subject to outstanding conditions.

However, courts have been willing to approve such schemes where the condition is clear, certain and fair, the status quo will be restored if the condition subsequent is not satisfied by a future specified date (which typically means the scheme will be terminated) and the condition does not introduce a new decision-making process after the court has approved the scheme.

The parties may agree at the time of signing the implementation deed that a regulatory approval will be dealt with as a condition subsequent. This was the approach adopted in the 2014 Xceed Resources / Keaton Energy acquisition scheme process. Alternatively, the parties may agree, post signing the implementation deed, to convert a regulatory condition precedent to a condition subsequent. This approach was adopted in the 2021 Redflex / VM Consolidated acquisition scheme process and the 2022 Afterpay / Block acquisition scheme process.

LEGAL AND COMMERCIAL CONSIDERATIONS INFORMING STRATEGY

When assessing the strategy to be adopted, key considerations will, of course, be each party’s ongoing assessment as to whether the approval will be obtained (including any conditions that might be imposed), the timetable for the regulator’s decision and the attractiveness of the transaction generally.

However, there are various other factors that will commonly bear upon the strategy of the bidder and target respectively:

Vulnerability of target directors’ and shareholders’ support for the transaction

Postponing the scheme meeting may heighten the risk of target directors changing their recommendation – say, because of a competing proposal that emerges or a fall in the bidder’s share price in the case of a scrip bid.

Equally, considerations such as these may make the support of target shareholders vulnerable.

From the bidder’s perspective, these considerations inevitably weigh in favour of obtaining shareholder and the court’s approval at the earliest opportunity.

From the target board’s perspective, engendering shareholder support for a recommended transaction, and a sense of momentum generally, will be important and may weigh in favour of putting the transaction to the shareholders and the court.

The same concern may apply to the bidder directors’ and shareholders’ support for the transaction, if bidder shareholder approval is required.

Potential for renegotiation of the transaction terms

A regulatory approval delay or failure may have an important bearing on the potential for renegotiation of the transaction terms.

An obvious illustration of this is a scenario in which an approval delay or failure is perceived as providing the bidder with leverage to negotiate a reduced price.

A critical issue in relation to potential price reductions in such a scenario is whether the scheme has already been voted on by shareholders at the scheme meeting.

If so, a price reduction will require shareholder approval, which may be very difficult to achieve as a practical matter.

From the target’s perspective, this practical difficulty may support a view that the optimal strategy is to obtain approval for the original price, notwithstanding that the regulatory approval has not been received, in order to preclude a renegotiation attempt. However, this potential benefit needs to be weighed against the risk that the practical difficulty leads the bidder to conclude that a price reduction is not viable and its interests are best served by terminating, rather than potentially proposing a reduced price that the target board may have recommended.

From the bidder’s perspective, this practical difficulty generally supports the view that the bidder should attempt any renegotiation before the scheme meeting. However, this may be unappealing for various reasons in the circumstances – e.g., it may not be possible to predict the outcome of the regulatory process, and its impact on value, with confidence at the relevant time.

The above discussion contemplates a scenario in which the regulatory approval is framed as a condition precedent.

If the regulatory approval is framed as a condition subsequent, a failure to satisfy the condition post the second hearing will result in the automatic termination of the scheme, thereby precluding any renegotiation.

Of course, a regulatory condition failure or other termination trigger may also facilitate a renegotiation attempt by the target.

Potential for additional termination rights to be triggered

Regulatory approval delay may also present the potential for termination rights other than a failure to satisfy the regulatory approval condition to be enlivened during the extended period to the scheme meeting and second court hearing.

A material adverse change termination right commonly draws attention when parties are considering what other rights could be triggered during an extended period. The MAC will typically be expressed to operate until the morning of the second court hearing.

From the target’s perspective, if an extended period to completion elevates the risk that the bidder will have grounds for asserting a MAC, this may weigh in favour of pressing ahead with the scheme meeting and the second hearing.

This carries with it the risk that the bidder concludes that renegotiation post the scheme meeting is not viable, as discussed above.

It may also encourage an attempt by the bidder to terminate on the basis that the MAC has already been triggered.

From the bidder’s perspective, if there was logic in consenting to the scheme meeting and second court hearing being held, it might be appropriate to press for an amendment to the implementation deed such that the MAC and other relevant termination rights continue to operate post the second court hearing.

Rights and obligations of the parties in relation to the regulatory approval process under the implementation agreement

The strength of each party’s contractual position in relation to the approval process under the implementation agreement will be central to their respective strategies.

Key clauses will include:

- The obligations of the target to proceed with the scheme meeting and second court hearing, particularly the flexibility given to the target in relation to the timing of these events.

Generally, these obligations are no more onerous than a reasonable endeavours obligation to meet an agreed timetable. - The “end date” by which the scheme must become effective and any obligation on the parties to discuss an extension to the date, or explore alternative transactions, in the event the scheme will not be effective by the agreed date.

- The efforts standards attaching to the obligation to secure the necessary approvals.

Notably, implementation agreements typically require a party to use “reasonable endeavours” to secure required approvals and that the approvals be obtained either unconditionally or on terms that the bidder (and potentially the target, in the case of a merger) considers acceptable acting reasonably.

Whilst we have seen an emerging trend of parties pre-agreeing conditions to an approval that must be accepted and it is common for the implementation deed to detail certain procedural steps required in connection with the obtaining of regulatory approval, “hell or high water”, litigation and other more specific efforts standards are not a common feature of the Australian market.

In that context, it is often debatable as to what is “reasonable” in the circumstances of a particular transaction, thereby complicating the strategic decision-making.

- The consequences of a party breaching its obligations in relation to the regulatory approval process or otherwise failing to secure the required approvals

If the only available remedy for breach by the bidder is an order for damages, this will not be much of an incentive for the bidder to perform, as the recoverable amount will generally be the financial loss suffered by the target company – i.e. usually just transaction costs and not the transaction premium that would have been received by target shareholders.

Of course, in the absence of a breach (say, because the approval is not obtained by the end date, notwithstanding the bidder satisfying its obligations), there will be no entitlement to damages.

Accordingly, targets now commonly obtain a reverse break fee that will be triggered by a material breach of the agreement (44% of agreed transactions in FY22) and potentially by a failure to obtain a regulatory approval (6% of agreed transactions in FY22).

However, the right to the fee triggered in those scenarios will only be as strong as the amount payable. Fees of 1% of transaction equity value are common in the Australian market and such amounts may act as an option fee (particularly if the agreement provides that it is the target’s sole remedy).

Acquisition financing considerations

Regulatory approval uncertainty or delay may place any debt financing for the acquisition in jeopardy.

Even where debt financing is in place on a certain funds basis, or the bidder otherwise got the target comfortable with the bidder’s ability to finance the transaction, at the time of signing the implementation agreement, a deterioration in debt markets generally or financier appetite for the particular transaction may be a significant factor informing the bidder’s and target’s approach.

Risk of shareholder approval going stale

At the second hearing, the court may need to consider whether the shareholder vote continues to reflect the views of the shareholders, if, for example, material new information arises after the vote.

The longer the period between the vote and the second hearing, the greater the potential for new material information to arise.

However, when considering whether to proceed with the shareholder meeting, the potential for this risk to crystalise needs to be assessed carefully in the context of the offer and the target’s particular circumstances.

For example, in the context of a fixed cash offer, the vote should remain valid in the absence of something that would make the target shares materially more valuable than the consideration on offer. A deterioration in the value of the target shares is unlikely to make the vote stale.

The potential for the chosen strategy to influence regulators’ timetables

Whilst regulators do not have a legal duty to satisfy the transaction timetables of parties, their timetables may at least be perceived to be influenced by whether the scheme meeting and the second hearing have been held (such that the regulator’s decision is delaying completion).

CONCLUSION

The determination of the optimal strategy to address an uncertain or delayed regulatory process typically involves an exercise of judgement and is often finely balanced.

Ultimately, we predict that, during the next 12 months, we will witness, on the part of bidders and targets, increasing focus being placed on the allocation of this risk before implementation agreements are entered into, driven by concern regarding approval timetables and economic conditions.

The proposed replacement of the Australia’s current informal merger clearance regime with a mandatory-suspensory notification regime would heighten this focus.

This may impact the negotiation of relevant rights and obligations under implementation agreements, such as those considered above.

Undoubtedly, it will lead to greater strategising, prior to the entry into implementation agreements, as to how to deal with uncertainty and delay.

Legal Notice

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2025

Stay in the know

We’ll send you the latest insights and briefings tailored to your needs