Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

The regulation of digital assets has been a topic of fierce debate in Australia and around the world in recent years. Alongside international developments in relation to the approach to regulating digital assets, Australian Government reviews have found that the risks associated with digital assets means that regulation is necessary. However, it is also a priority that this regulation is approached in a manner that promotes innovation.

While previous governments took steps to propose digital asset regulatory reform, the current Government started afresh in early 2023, with a token mapping exercise. With the release of the ‘Regulating Digital Asset Platforms’ paper (Proposal Paper) in October 2023, we now have better insights on how the Government proposes to regulate digital asset connected services in Australia.

The Proposal Paper outlines a regulatory framework with the following key features:

The development of a framework in relation to digital assets is not being made in isolation. Rather, it is part of a much bigger focus by the Australian Government to modernise Australia’s financial systems and ensure that financial regulation remains fit for purpose in the face of evolving technologies and markets.

The key proposal of the paper is to bring certain digital asset connected activities within scope of the AFSL framework under the Corporations Act. To do so, it is proposed that:

This is a clear change in direction compared to what may have been expected following the token-mapping exercise undertaken earlier in 2023. This exercise seemed to indicate that a token-based/technology-based approach was going underpin any regulatory framework. However, this new approach to regulation focuses instead on risks created by intermediaries in the digital asset ecosystem, rather than the digital assets themselves. The approach is intended to create consistent regulatory outcomes regardless of the underlying token or technology while focussing on where the potential harm might be.

In our view, this is a considered and nuanced approach to regulation in connection with digital assets. As digital asset technologies are constantly evolving, an activities and risk based approach is better suited to ensuring that any regulatory framework remains adaptable to the evolving and entrepreneurial digital asset market.

The Proposal Paper suggests a regulatory framework that is contingent on there being a DAF. It also introduces a new concept of ‘financialised functions’. We have examined these concepts below.

(i) What is a DAF?

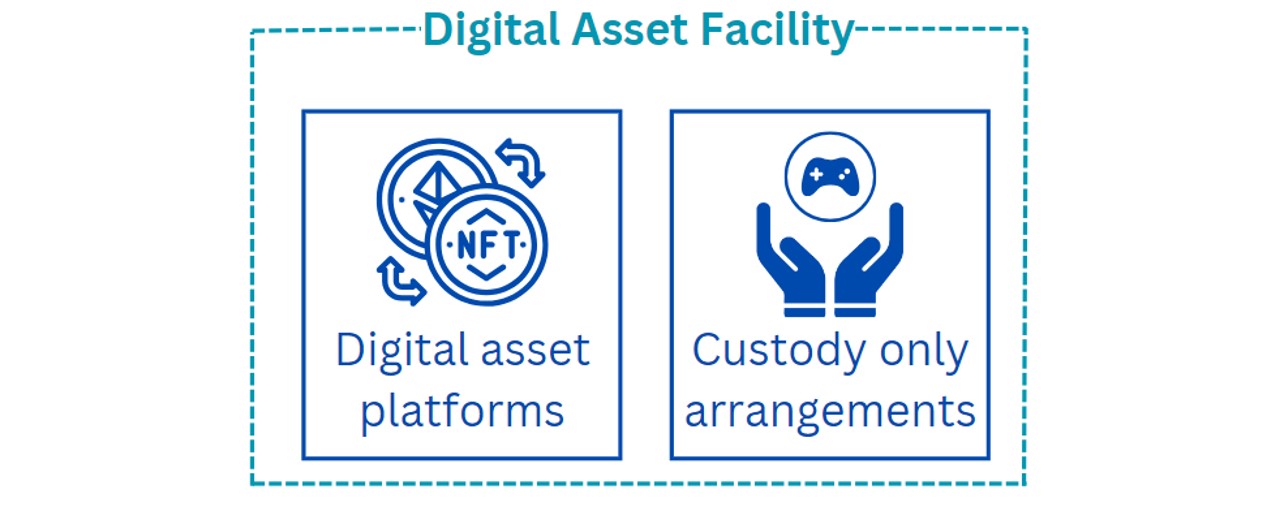

Description of a DAF

A DAF is described in the Proposal Paper as an:

‘asset holding arrangement’.

It would cover:

Consideration of control

While the description of a DAF is based on an asset “holding” arrangement, the Proposal Paper provides that the framework would leverage concepts of “control” to determine what amounts to a DAF. The Proposal Paper provides that businesses within the regulatory perimeter would include those:

‘with the ability to exercise, coordinate, or direct ‘factual control’ over the assets in a real and immediate sense’.

The Proposal Paper specifically identifies businesses claiming to provide ‘decentralised finance’, which in fact have the ability to exercise control over digital assets, and perpetuate frauds and scams in doing so, as a target of these reforms.

(ii) How the AFSL Framework applies to DAFs under the proposal

As is the general approach under the Corporations Act, it is proposed that the existing AFSL regime will apply to any person ‘carrying on a financial services business in Australia’ in relation to a DAF.

‘Financial services’ for this purpose include:

The standard obligations under Chapter 7 will apply to those providing financial services in relation to a DAF.

Given that DAFs are financial products under the proposed regime, rather than the tokens themselves, an entity will only be providing financial product advice when the entity is giving advice about using a DAF and/or investing through it. The Proposal Paper suggests that DAF advice would include advice in relation to acquiring, holding and disposing of digital assets (both financial product and non-financial products) through a digital asset platform.

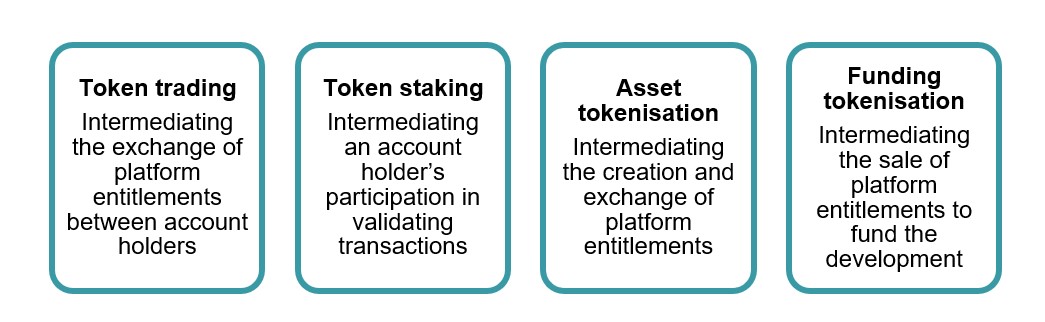

(iii) ‘Financialised Functions’

A notable feature of the Proposal Paper is the introduction of ‘financialised functions’ into the proposed digital assets regulatory regime. Given that the reforms are at consultation stage, there are aspects of the regime that will become clearer with draft legislation. However, the Proposal Paper is clear that the regulation of financialised functions is not contingent on there otherwise being a financial product involved.

Financialised functions would cover the following:

As suggested above, the proposed framework captures a broad range of activities where an entity is carrying on a financial services business in relation to a DAF. We have outlined certain illustrative scenarios of how the framework may apply in practice below.

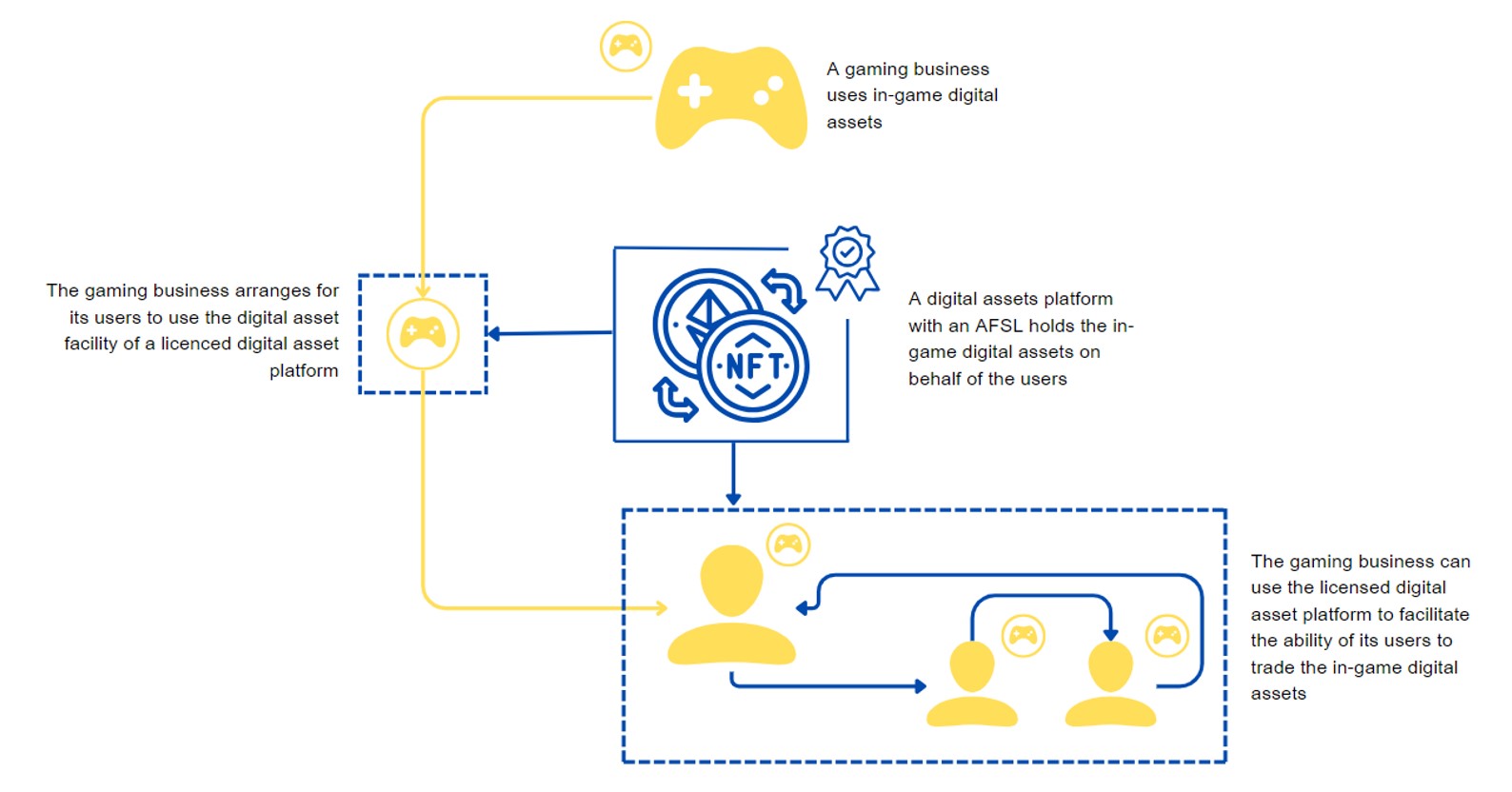

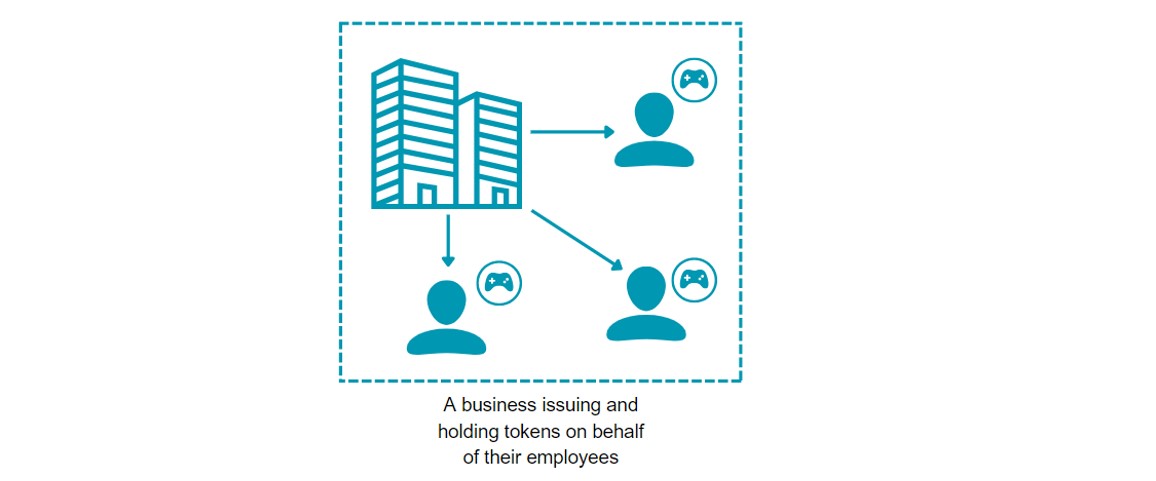

The proposed DAF regime would regulate those providing financial services in connection with DAFs. As the concept of a DAF is broad, any business that has control of digital assets of another person would be providing a DAF. For example, a gaming business may hold tokens on behalf of its users where those tokens are used as part of the game. In this scenario, the holding of those digital assets would be considered a DAF and the gaming business would need to hold an AFSL.

The proposed framework suggests that this should be addressed by the non-financial business appointing an AFSL holder to hold the digital assets. The non-financial business would be exempt from holding an AFSL, which would otherwise be required to “advise” on or “arrange for” the issuance of the DAF, if the following is satisfied:

This would mean that the gaming business would not be able to retain control over the digital asset (as this would be issuing a DAF) and control of the digital assets must sit with an AFSL holder.

How might the non-financial business exemption work in practice?:

This exemption, as currently contemplated in the Proposal Paper, requires that the non-financial business deal only with licenced “platform providers”. As noted above, DAFs may exist in relation to both digital asset platforms and custody only arrangements. We expect that the exemption would be intended to capture custody only arrangements if appropriately licensed.

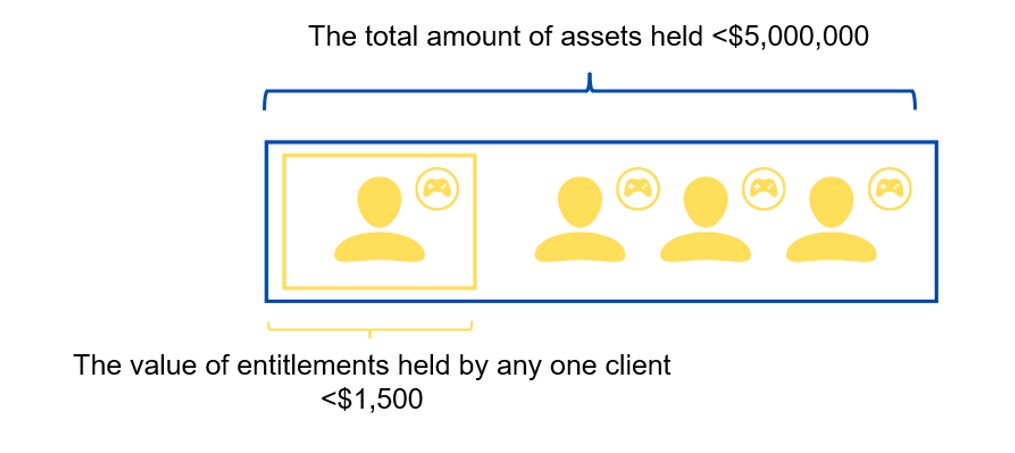

Another exemption has been proposed for entities that deal in low-value digital asset facilities. Much like the exemption available to low value non-cash payment facilities, this exemption is proposed to allow businesses to hold digital assets for others without needing an AFSL if the value of those digital assets fall below certain monetary thresholds.

The form of this exemption would need to be carefully considered in order to be effective and useful in the context of digital assets. For example, digital assets may be utilised by businesses for a variety of reasons that are valuable to that business for security or data integrity reasons. However, those digital assets may not otherwise have value outside of that business.

In addition, the value of digital assets can be highly volatile and uncertain. Any exemption for low value DAFs would therefore need to be framed having regard to the fact that there may not be a clear market value for all digital assets at all times and that this value may change significantly and swiftly on an ongoing basis.

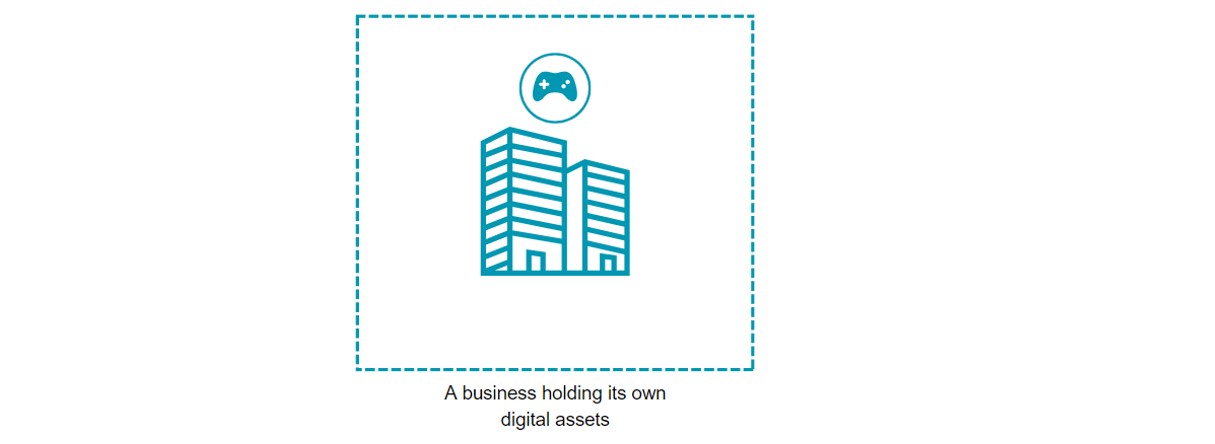

The Proposal Paper does not expressly consider how the framework would apply (if at all) to companies or other corporate structures utilising digital assets within their own businesses.

For example, a business may possess the relevant resources and expertise to internally develop, issue and hold digital assets and tokens for employees. At this stage, it is unclear whether this would constitute a DAF for the purposes of the digital asset framework or, alternatively, whether utilising digital assets in this way is intended to be captured by the scope of the framework at all.

However, on the basis that the digital assets are created and controlled by the entity using those assets, there should be no DAF as control sits with the owner of those digital assets.

The proposed digital assets framework is only one part of the Government’s Strategic Plan and other regulatory priorities. Proposed regulatory changes for payments and reform to the AML/CTF Regime have also been released for separate consultation. Alongside these, this Proposal Paper makes it clear that the Government intends to introduce major reforms that will have significant impacts for Australia’s digital assets regulatory framework.

Submissions in response to this paper have closed. However, if you would like any assistance in relation to any of the proposals in this paper, or would like to discuss the other regulatory reforms currently in progress, please reach out to us.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2025

We’ll send you the latest insights and briefings tailored to your needs