Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

The transition to cleaner technologies such as solar and wind power, battery storage and electric vehicles has prompted a global surge in forecast demand for critical minerals over the coming years.

The need to increase exploration, extraction and recycling of critical minerals is mostly understood. However, questions of the security of the wider critical mineral supply chain, product provenance and ESG credentials are coming to the forefront, in particular in light of new regulatory developments, including the EU's recent Batteries Regulation and proposed Critical Raw Materials Act.

Critical minerals need to be refined (often using highly complex processes) before they are fit for end use. Processing is currently dominated by a handful of countries. A recent survey by the International Energy Agency found that just three countries controlled between 80 – 99% of the processing of lithium, cobalt and rare earth elements, with China alone controlling 58% of lithium, 65% of cobalt and 87% of rare earth elements global processing capacity.1

This imbalance creates a serious risk of supply chain bottlenecks, geopolitical risk and price volatility, which has prompted governments around the world to commit to increasing their domestic critical minerals processing capacity. This will create considerable opportunities for both debt and equity investment in new processing projects and technologies, with project finance expected to play a major role.

In this briefing, we look at some of the key considerations for financing critical minerals processing projects.

|

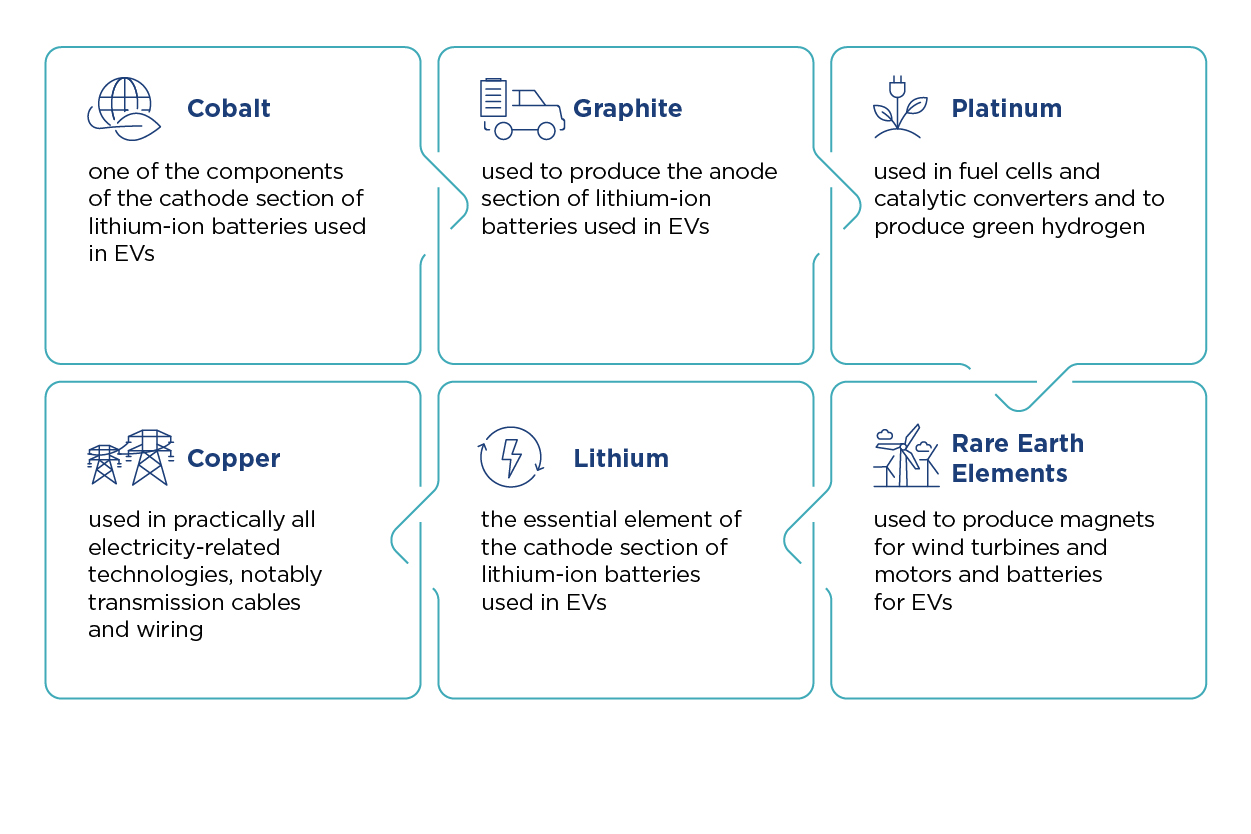

What are critical minerals? Although there is no universal definition, critical minerals all share two key characteristics: (i) they are seen as indispensable to particular technologies (in particular, in the energy, defence and healthcare sectors) and (ii) they are subject to a perceived risk of supply chain disruption. The following is a non-exhaustive list of what are currently commonly regarded as critical minerals and some examples of their uses:

|

There is a clear trend towards "green" refining projects as ESG requirements and geopolitical risk mean that not all product is equal and price is not the only consideration.

Critical minerals processing is usually very energy-intensive, especially where the underlying feedstock has a low mineral content, and can also require large volumes of water and produce hazardous waste.

Processing companies are facing growing pressure from stakeholders to address these and various other environmental and social-related issues. Foremost among those stakeholders are the original equipment manufacturers (OEMs) and other end users, who are new entrants into the sector and are bringing a whole new set of commercial objectives to traditional offtake and financing transactions.

Important considerations for sponsors planning a "green" project will include:

Sponsors will also need to be alive to the risk of overstating the project's green credentials, with the potential for litigation and regulatory action in respect of any perceived "green washing".

OEMs are themselves subject to increasingly onerous legislation on supply chain due diligence, such as the German Supply Chain Act (that came into force on 1 January 2023) and the EU Batteries Regulation (that came into force on 17 August 2023). These rules require ongoing monitoring and mitigation of ESG risks throughout critical minerals supply chains, including the processing stage.

OEMs are also required to produce detailed information on the provenance and carbon footprint of each of their manufacturing inputs. To facilitate this, independent third party certifications, such as Initiative for Responsible Mining Assurance (IRMA) for mining companies, and block chain verification are expected to become the norm for processing companies.

Requirements of this kind require significant access and information flows between processing companies and OEMs, as well as ongoing operational cooperation on ESG risks. In our experience, both groups are still coming to terms with the challenges – and mutual benefits – of this new relationship.

Significant investment will be required to meet the battery metals processing requirements of the European gigafactory build out, and further investment needed for the critical minerals required in other energy transition sectors.

There is potential for funding for processing projects from a variety of sources, including:

A key concern for any processing plant will be ensuring security of supply of feedstock.

Processing projects which also own mines for the relevant feedstock are protected against supply risk in a market where long term supply contracts are currently uncommon. Vertically integrated projects are also better placed to manage feedstock price fluctuations, but are subject to "project-on-project" risk if the mine is being developed at the same time as the processing plant.

For processing-only projects, investors and financiers will want to ensure (among other things):

The pricing mechanism for the feedstock will be another important consideration for processing-only projects, since the project will be exposed to a cost / revenue squeeze if price increases for the feedstock are not matched by increases in price for the processed product (as is sometimes seen).

There are a number of ways to mitigate this potential pricing mismatch, including:

Certainty of revenue stream (through the sale of the processed product) is another key bankability consideration.

Long-term offtake contracts featuring "take or pay" provisions, of the type traditionally favoured by lenders in the mining sector, are not currently widely available in the critical minerals processing market. OEMs have favoured short term supply agreements (or supply agreements which are subject to termination at short notice), an exception being where the OEMs purchase product as part of a broader investment package in the project.

In our view, if the project has a product supply agreement with a reputable, financially strong counterparty and there is a clear and firm commitment to take product and pay for it at designated times, then this may be sufficient from a bankability perspective without requiring the additional contractual overlay of "take or pay" protection.

Further, if there is resistance from buyers to enter into long term product supply agreements, "evergreen" provisions can be included under which the relevant contract will rollover for a further term unless an extended period of notice is given by the buyer to terminate (that extended notice period would then give the processing company, as seller, time to arrange the sale of product to, and commence product qualification arrangements with, a substitute buyer).

Lenders will usually also wish to see downside protection in relation to the product price, so that the price achieved always supports the revenue assumptions in the financial model. This can be achieved in a number of ways:

As with feedstock supply contracts, lenders will want the termination events under the product sale agreements to be as limited as possible, and may also require direct agreements for key offtake contracts.

Buyers will typically require that the processed product go through a series of qualification tests before fully committing to purchase on extended contractual terms. These tests can include matters which are outside the processing company's control, are described only vaguely, and will take an extended period to satisfy. If the product does not satisfy the relevant tests, the consequence can be rejection of product and early termination of the offtake contract.

Having robust technical solutions is the best protection against these risks, but the processing company should also aim to ensure that the qualification tests are as objective (and of short duration) as possible, with appropriate remedy periods for failure to satisfy the tests.

Product which does not meet the required specification (e.g. battery grade) will most likely be able to be sold as a lower grade material, which should be taken into account in the project cashflows for the purposes of the financial model.

From a bankability perspective, the construction contracting strategy for the processing plant should:

Lenders (through their technical and market advisers) will want to make sure that the project's chosen processing technology is appropriate, taking into account, among other things, the type (and quality) of feedstock, the processed products produced by the plant, alternative technologies available in the market (for both the processing operations and the relevant manufactured end products) and any product recycling requirements.

Where the proposed processing technology is new (or is established technology that is being used in an innovative manner), conformity to local industry standards and regulations will be an important consideration. In these circumstances, contractors may also be reluctant to accept strict fitness for purpose obligations and may seek additional exclusions from liability (including regarding performance guarantees) or, possibly, lower than usual caps on liability.

The by-products from the processing operations can be an additional revenue stream for processing companies if there is a market for them. For example, gypsum, which is one of the by-products from the lithium hydroxide production process, is used widely in the construction industry in cement and plaster products.

Perhaps just as significantly, the sale of by-products can also be a useful way for processing companies to demonstrate their green credentials (e.g. in relation to the disposal of waste).

Sponsors may look to expand the project's processing capacity in the future by adding additional processing lines or "trains", as this can sometimes significantly improve a project's IRR for a comparatively lesser cost.

Where expansion is contemplated day-one, the finance documents may include in-built accordion arrangements or permitted financial indebtedness for this purpose. Lender consent will be required, and before giving approval, lenders will want to be satisfied the original plant is performing (and has established a firm track record) and the financial ratios will not be adversely impacted by the expansion.

We have considerable experience advising on projects across the critical minerals value chain. If there are any points in this article you would like to discuss, please feel free to get in touch with any of the key contacts below.

For more information on financing the energy transition, see our previous articles in this series on smart meters and battery storage.

A version of this article also features in Project Finance International, attributed to partners Helen Beatty and David Walton, and senior associate Thomas Papworth. Helen Beatty and Thomas Papworth were also quoted in Global Trade Review's article 'Before the white gold rush', which discusses how banks, corporates and governments worldwide are responding to the need for financing as the critical minerals sector develops.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills 2025

We’ll send you the latest insights and briefings tailored to your needs